Before starting the process of applying for a mortgage, it's vitally important your advisor has access to all the relevant paperwork.

Not only will it allow them to fully understand your circumstances and seek clarification where required, but it means you'll receive your mortgage offer more quickly as well.

With that in mind, we've put together this handy checklist of self-employed mortgage documentation. We recommend you bookmark it for easy access.

Income proof for a self-employed mortgage

To get a self employed mortgage, you must be able to prove both your business profits, and individual income. Most lenders want to see at least 2 years worth of accounts, though a few will work with just one.

Standard documentation to verify income

If you're a sole trader, LLP equity partner or company director, you'll need to provide the following documents for each of the past 2 years , where you've been trading that long:

- Business, partnership or company financial accounts, produced by a qualified accountant*

- SA302 tax calculation

- Tax year overview (TYO)

*If you don't use an accountant, let us know so we can advise you.

Accountant's certificates

A few lenders will accept an accountant's certificate, in lieu of the SA302 and Tax Overview documents. The certificate is a form signed by your accountant verifying business turnover, gross and net profit before tax for sole traders, and post-tax profit, salary and dividends for directors.

Documentation to provide if you're a contractor

Contractors must provide their current contract, sometimes in addition to the documents listed above.

If your earnings are high enough, and/or you fit the lenders other criteria, it's often possible to be treated as employed for income assessment. In which case, your contract and bank statements can be sufficient to evidence your income.

If you contract through an umbrella company, you'll need to provide your contract and P60s for the past 2 years (where available).

What's an SA302?

An SA302 is an official tax calculation document produced by HMRC after you submit your personal tax return (SA100).

Aside from showing how much tax you owe, the SA302 summarises your declared earnings for the tax year, including pre-tax profits for sole traders, and salary and dividends for company directors.

Other income streams such as investments or rent are also included.

How do I get my SA302?

If your accountant uses commercial accounting software to submit your self-assessment tax return, they should provide you with the tax calculation, or tax computation as it's also known.

This is essentially an unofficial version of the HMRC's SA302 tax calculation, but it's widely accepted by lenders for mortgage purposes.

Even though they are not strictly the same thing, you'll often see the terms SA302 and tax calculation/computation used interchangeably. The latter is often, but not always, referring to the accountant supplied version. Rule of thumb: if you have an accountant, ask them to provide your tax calculation.

If you or your accountant filed your tax return directly via HMRC Online, your SA302 should be ready to print as a pdf file 72 hours later.

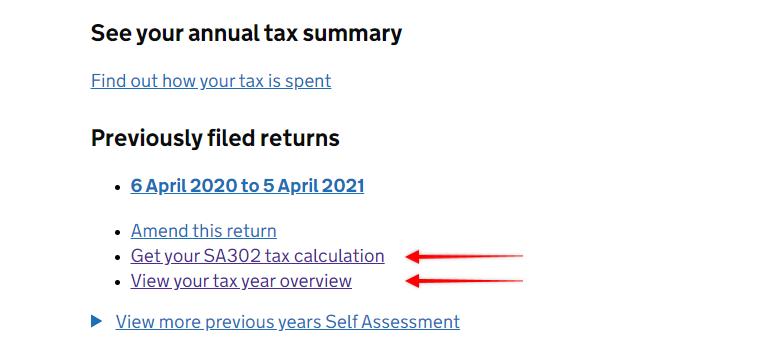

To print your SA302:

- Sign into your HMRC Login account

- Go to 'Self Assessment'

- Scroll down the page to 'Previously filed returns'

- Click Get your SA302 tax calculation

- Select the SA302 for the relevant year

- Select 'Save as PDF' and click Save

What's a Tax Year Overview?

The Tax Year Overview (TYO), or Tax Overview as it's sometimes called, is a document produced by the HMRC. It verifies the figures in your SA302 are correct, and shows the tax to be paid by yourself or refunded by HMRC.

The SA302/tax calculation and TYO go hand in hand, and for mortgage purposes, most lenders will want to see both documents for the relevant year(s).

How do I get my Tax Year Overview?

Downloading your TYO documents from HMRC is very similar to how you accessed your SA302s.

To print your Tax Year Overview:

- Sign into your HMRC Login account

- Go to 'Self Assessment'

- Scroll down the page to 'Previously filed returns'

- Click 'view your tax year overview'

- Choose the year from the 'Tax year ending' dropdown menu and click Go

- Click 'Print your tax year overview'

- Select 'Save as PDF' and click Save